Regarding the matter of legal bailments, in this blog we take a close look at Bredenkamp v Gas Sensing Technology Corporation (GSTC), in the matter of Welldog Pty Ltd (In Liq) (Receivers and Managers Appointed) [2017] FCA 1065.

While the outcome of this case is interesting, all bailment circumstances are different. So please don’t hesitate to seek advice from our Sydney business lawyers on 1800 770 780.

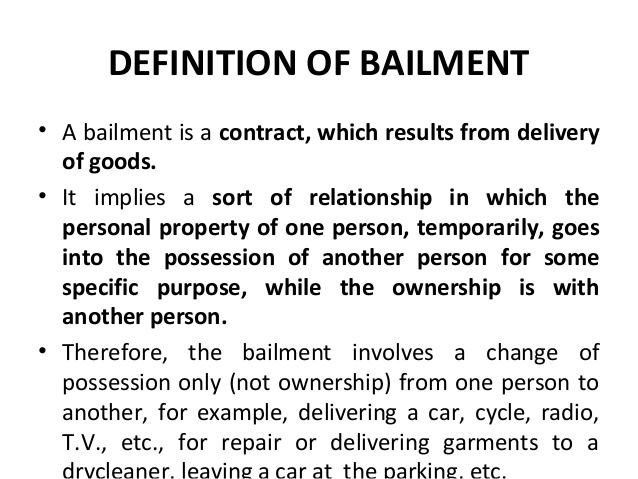

What is bailment?

Bailment is a legal relationship in common law where physical possession – but not ownership – of personal property, is transferred from one person to another.

What happened in this case?

GSTC, a US company, provided product line management and research and development services.

It was common for its Australian subsidiary, Welldog, to store equipment shipped from GSTC in the US, to be used by GSTC subsequently when work was to be done by GSTC in Australia. This happened on at least four occasions. The equipment was stored at the Toowoomba base of Welldog Australia. It was not in dispute that Welldog had possession of the equipment.

GSTC conducted its own operations in Australia, often alongside Welldog. Receivers were appointed to Welldog which subsequently passed into administration and liquidation. The liquidator sought to retain possession of the goods (equipment) for the benefit of unsecured creditors, arguing that it was the subject of a PPSA lease under s 13 of the Personal Property Securities Act 2009 (PPSA) requiring registration to avoid the application of s 267 of the PPSA.

The Receivers, on the other hand, argued that the arrangement could only be a PPS lease if it was a bailment for value and the bailor (GSTC) was regularly engaged in the business of bailing goods – s 13 (2) (b) PPSA. The facts of the case pre-date the May 2017 amendments abolishing the stipulation in section 13(1)(b) that a bailment for an indefinite term is a PPS lease.

Was there a bailment?

GSTC could demand return of the equipment to it or to its employees or agents, at any time. There was no contractual arrangement for example, by which Welldog could insist on retaining possession of the property.

Such arrangements where the bailor can at any moment demand return of the object ‘bailed’ are called gratuitous bailments.

But Welldog did not hold the equipment exclusively for GSTC. Some of the equipment which was stored was used by Welldog, even though other parts, or sometimes even the same parts, were used by GSTC. Nevertheless, the court concluded that the facts still qualified the arrangement as a common law gratuitous bailment despite the fact that Welldog did not hold the equipment exclusively for GSTC.

Was GSTC regularly engaged in the business of bailing “personal property”?

The equipment was stored by Welldog while GSTC was in transit between jobs or tasks. Once a new project or task arose for GSTC, for which the equipment could be used, GSTC collected the equipment and used it for that purpose.

In addition, GSTC had geochemically characterised hundreds of oil and gas wells around the world. But the storage of the equipment with Welldog had only occurred 4 times. Moreover, the storage of the equipment by Welldog arose in an ad hoc fashion. It was not a normal part of GSTC’s business. Taking these facts into account, the court concluded that GSTC was not regularly engaged in bailing the equipment (s13(2)(b)).

GSTC said that it profited from supplying services to clients using its skilled personnel and its equipment. It did not profit from the bailing of equipment to Welldog or to the clients of Welldog. GSTC did not pay Welldog a fee for the bailment and even if it did, the fee would merely be an incidental expense to its business and not the business itself.

GSTC did not bail the equipment for Welldog’s use. Welldog occasionally used or exploited the equipment and got income from doing so, which could have resulted in some payment to GSTC (Welldog being its subsidiary) and therefore some profit being made by GSTC. However, there was no ‘business model’ whereby GSTC made its money by placing the relevant equipment with Welldog.

The court said at [109] that it was more appropriate to describe the financial outcomes derived by Welldog from use of the equipment as arising pursuant to a service provision arrangement whereby the parent company assisted its subsidiary, rather than an indication that the parent company (GSTC) had bailed goods to Welldog as part of a bailment business.

The court concluded that GSTC was not in the business of bailing goods, as required by s 13(2)(b) of the PPSA.

Did Welldog provide value for the bailments?

This element is required by s 13 (3) of the PPSA. The court considered it in the event that its conclusion as to the application of s 13 (2) (b) was wrong.

The word ‘value’ as used in s 13 (3), is defined in s 10 and

- a) means consideration sufficient to support a contract; and

- b) includes an antecedent debt or liability.

GSTC charged Welldog a management fee for the assistance it provided Welldog and whilst Welldog issued invoices to GSTC for the completion of works using the equipment, no specific charge was invoiced to GSTC by Welldog for the bailments.

However, the receivers argued that this was not to the point. The issue according to the receivers, was whether looking at the entire nature of the bailment relationship, value was given by Welldog as bailee, to GSTC as bailor. In other words, the receivers argued that “value” meant “value at large”.

It was clear that Welldog derived a benefit by reason of the equipment being at the Welldog premises. And it was Welldog’s obligation to ensure that the equipment was safely and securely stored in its secured premises. But it was not disputed that Welldog did not provide any specific value to GSTC for the bailment.

The court said that mere storage of the equipment safely and maintaining it in good working order was not evidence of value being provided by Welldog for the bailment. The court said it was to be expected of a subsidiary that it would keep the equipment of its parent safe even if it is not a bailee.

The court concluded that whilst the provision of relevant equipment by GSTC to Welldog was to enable Welldog to conduct its business with financial benefit potentially flowing to GSTC, value of such indirect nature, including the management fee, does not satisfy the statutory concept of “value” as appears in s 10.

The court supported its conclusion by stating that the consideration was quite uncertain and it was too indirectly related to the provision of the equipment to support the ready conclusion that the equipment was bailed for such benefits.

His honour was guided by the New Zealand Rabobank and the Western Australian Re Arcabi decision in coming to this conclusion.

Conclusion

If you are in the business of hiring or consigning your goods, or you otherwise part with possession of your inventory before payment, then give Leigh Adams a call on 1800 770 780. He can review your arrangements to minimise the chances of losing it to your customer’s liquidator. As one of the most experienced commercial law firms Sydney has to offer, we are well equipped to handle any and all of your civil litigation issues.